Navigating the Jewelry Overload: A Comprehensive Guide to Debt-to-Income Ratios

Related Articles: Navigating the Jewelry Overload: A Comprehensive Guide to Debt-to-Income Ratios

Introduction

With great pleasure, we will explore the intriguing topic related to Navigating the Jewelry Overload: A Comprehensive Guide to Debt-to-Income Ratios. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating the Jewelry Overload: A Comprehensive Guide to Debt-to-Income Ratios

In the realm of personal finance, understanding your financial health is paramount. One crucial metric that offers a clear snapshot of your financial standing is the debt-to-income ratio (DTI). While the concept of DTI is fairly straightforward, its application to the world of jewelry can be less clear. This article delves into the intricacies of "jewelry overload" and its impact on your DTI, providing a comprehensive guide to navigate this potential financial pitfall.

Defining Debt-to-Income Ratio (DTI)

The debt-to-income ratio (DTI) represents the percentage of your monthly gross income that is allocated to debt payments. It is a crucial indicator of your financial capacity and plays a significant role in various financial decisions, including loan approvals, creditworthiness, and overall financial stability.

Calculating Your DTI:

To calculate your DTI, follow these steps:

- Determine your total monthly debt payments: This includes all recurring debt obligations such as credit card payments, student loans, car loans, mortgages, and personal loans.

- Calculate your gross monthly income: This is your income before taxes and deductions.

- Divide your total monthly debt payments by your gross monthly income: Multiply the result by 100 to express the ratio as a percentage.

Example:

Let’s say your total monthly debt payments are $1,500 and your gross monthly income is $5,000. Your DTI would be calculated as follows:

- $1,500 (Debt Payments) / $5,000 (Gross Income) = 0.3

- 0.3 x 100 = 30%

Therefore, your DTI would be 30%.

Jewelry Overload: A Potential DTI Culprit

While jewelry can be a source of joy and personal expression, it can also become a financial burden if not managed responsibly. "Jewelry overload" refers to a situation where excessive spending on jewelry significantly impacts your DTI, potentially leading to financial strain.

Factors Contributing to Jewelry Overload:

Several factors can contribute to an inflated DTI due to jewelry purchases:

- Impulsive buying: Making spontaneous jewelry purchases without considering their financial implications can quickly lead to debt accumulation.

- Emotional spending: Jewelry can be an emotional purchase, often associated with celebrations, milestones, or self-indulgence. This can lead to overspending when emotions override financial prudence.

- Keeping up with trends: The ever-changing fashion landscape can create pressure to purchase new jewelry, leading to an accumulation of pieces that may not be truly cherished.

- High-interest financing: Utilizing credit cards or installment plans to purchase jewelry can lead to significant interest charges, further increasing your DTI.

- Lack of a budget: Without a clear budget and spending plan, it’s easy to lose track of jewelry expenses, leading to an inflated DTI.

The Impact of Jewelry Overload on DTI:

A high DTI due to excessive jewelry spending can have several negative consequences:

- Loan denials: Lenders often use DTI as a crucial factor in evaluating loan applications. A high DTI may result in loan denials or higher interest rates.

- Credit score decline: Excessive debt payments can negatively impact your credit score, making it more challenging to secure loans or credit cards in the future.

- Financial stress: High DTI can create financial stress and anxiety, impacting your overall well-being.

- Limited financial flexibility: A significant portion of your income allocated to debt payments reduces your financial flexibility to pursue other financial goals, such as saving for retirement or investing.

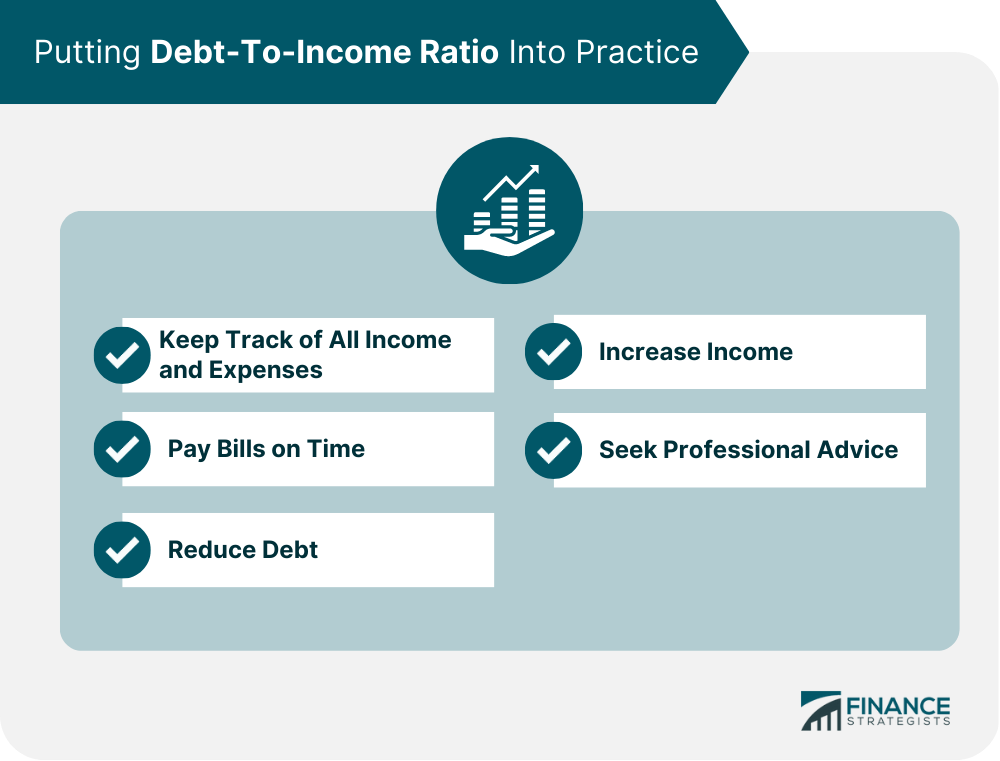

Navigating Jewelry Overload: Strategies for DTI Management

To avoid jewelry overload and its negative impact on your DTI, consider the following strategies:

- Develop a Budget: Create a detailed budget that allocates a specific amount for jewelry purchases. This allows you to track your spending and avoid exceeding your allocated limit.

- Prioritize Needs over Wants: Before making a jewelry purchase, consider whether it is a true need or a want. Focus on essential expenses and allocate discretionary spending wisely.

- Practice Delayed Gratification: Instead of making impulsive purchases, give yourself time to consider the purchase and determine if it aligns with your financial goals.

- Shop for Value: Explore affordable jewelry options without compromising on quality. Consider purchasing secondhand or vintage jewelry to find unique pieces at lower prices.

- Avoid High-Interest Financing: Opt for cash purchases or explore alternative financing options with lower interest rates. Avoid using credit cards or installment plans for jewelry purchases unless absolutely necessary.

- Seek Financial Guidance: Consult with a financial advisor to develop a personalized financial plan that addresses your spending habits and financial goals.

FAQs: Jewelry Overload and DTI

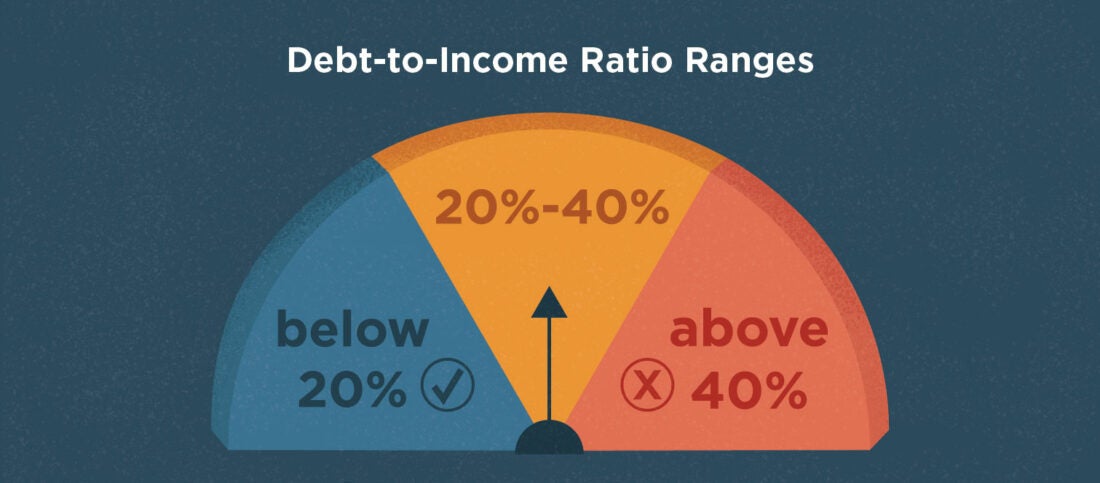

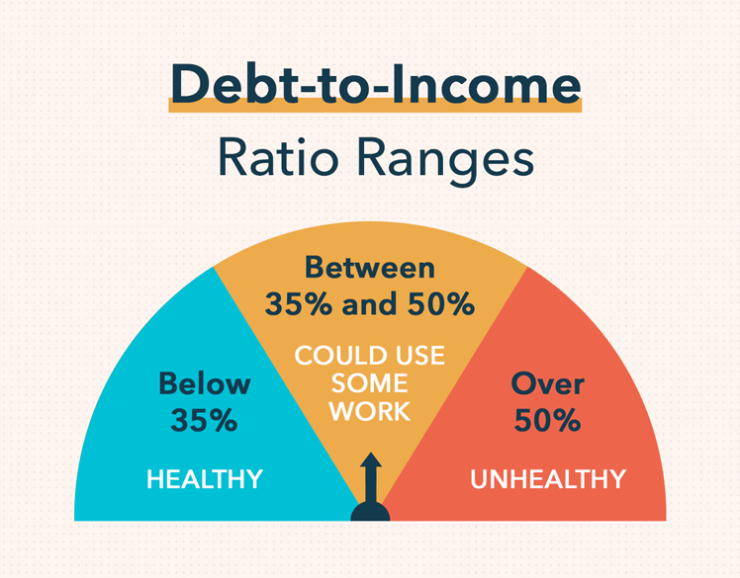

Q: What is a healthy DTI?

A: A healthy DTI is generally considered to be below 36%, with a lower DTI being more favorable. Lenders often use this threshold as a guideline for loan approvals.

Q: How can I reduce my DTI if it’s high due to jewelry purchases?

A: You can reduce your DTI by:

- Consolidating debt: Combining multiple debts into a single loan with a lower interest rate can lower your monthly payments.

- Making extra payments: Paying more than the minimum payment on your debts can help you pay them off faster and reduce your DTI.

- Negotiating lower interest rates: Contact your creditors to see if they are willing to lower your interest rates.

- Selling unwanted jewelry: Selling jewelry you no longer wear can help you generate funds to pay off debt and reduce your DTI.

Q: Should I avoid buying jewelry altogether?

A: Buying jewelry is not inherently bad. However, it’s crucial to be mindful of your spending habits and ensure that jewelry purchases do not negatively impact your DTI or overall financial health.

Tips: Jewelry Overload and DTI

- Set financial goals: Define your financial goals and ensure that your jewelry purchases align with these goals.

- Track your spending: Monitor your jewelry spending to identify any areas where you may be overspending.

- Consider the long-term impact: Before making a jewelry purchase, think about its potential impact on your finances in the long run.

- Seek support: If you struggle with impulsive jewelry buying, consider seeking support from a financial advisor or a support group.

Conclusion: A Balanced Approach

Jewelry can be a cherished possession that adds joy and personal expression to our lives. However, it’s crucial to approach jewelry purchases with a balanced perspective, considering their impact on your DTI and overall financial well-being. By developing a budget, prioritizing needs over wants, and practicing responsible spending habits, you can enjoy the beauty of jewelry while maintaining financial stability. Remember, a healthy DTI is a key indicator of financial health, and a mindful approach to jewelry purchases can contribute to a brighter financial future.

Closure

Thus, we hope this article has provided valuable insights into Navigating the Jewelry Overload: A Comprehensive Guide to Debt-to-Income Ratios. We thank you for taking the time to read this article. See you in our next article!